FoodStuff by Kevin Ryan

Why CPG can't do moonshots anymore

Here is a link to my last newsletter, in case you missed it.

In this week’s newsletter:

Over-Hyped: Is Personalization a Dead End?

Failure to Launch: Why CPG can’t do moonshots anymore

Extraordinary Ordinary : Premiumizing the Everyday

New Product Gut Reaction: The WOW! and the WHAT?

TIDBITS: Fun and interesting news from the world of food and the food industry

Maybe We Are Making Personalization Too Complicated?

Fast food chain Sonic has a new campaign titled “Make It Dirty” to introduce their new soda add-in, a coconut, cream and lime shot. The add-in can be combined with any of Sonic’s beverages for an additional $1.30. Made popular by companies like Swig, dirty sodas have become a hot trend on social media.

Coffee Mate (a Nestle brand) has partnered with Dr. Pepper to create a new Coconut Lime creamer specifically to be used to make a “Dirty Soda.” Consumers pour the creamer into their Dr. Pepper to recreate a dirty soda at home. Available at nationwide retailers.

Hidden Valley Ranch (a Clorox brand) is introducing a new line of Secret Sauces based on the popular seasoning. The company describes the four new products as ‘restaurant-style’. Available as Taco, Burger, Seafood, and Chicken.

Chocolate company Endangered Species is introducing a new snack option in their portfolio. Dip ‘n Joy are small batons of chocolate along with a sidecar of peanut butter, almond butter, or salted caramel. Available at retailers across the US.

So What? For years now, every CPG company has been trying to figure out personalization. Companies are spending millions to ‘crack the code’ and deliver to consumers bespoke products using complex databases, mobile phone integration, and DTC ventures.

However, what if was just as easy as nondairy creamer shots added to regular soda?

The more I look at personalization, the less I’m convinced that consumers really want the full package. Yes, the idea of getting a meal customized to your DNA or unique tastes sounds intriguing, but the cost and inability to share in the collective enjoyment (i.e., “Have you tried that Spicy Calabrian Sauce from Roe’s? What did you think?), is too often overlooked.

Instead, I think we are seeing the growth of personalization through controlled choice. What dirty soda, HVR Secret Sauce, and dippable chocolate have in common is that they allow the user to decide on how indulgent they want their experience to be while still being easily available. For example, while most people aren’t having a milkshake every day, dirty soda can turn an ordinary beverage into a daily treat. Similarly, the new Nestle product allows consumers to dial in the decadence to their specification.

I think the rise in popularity of sauces in general is due to this trend. Choosing MY sauce makes an affordable burger more unique to me while still allowing me to try the same burger everyone else is raving about (no need to personalize the whole thing). Plus, I can then choose the amount of sauce to add, making it lean or indulgent with just a squeeze.

Are we ever going to achieve ‘just for you’ personalization? Maybe we don’t need to? Maybe the idea of total personalization was a solution dreamed up by companies in need of a problem?

Why Can’t Big CPG Do Moonshots Anymore?

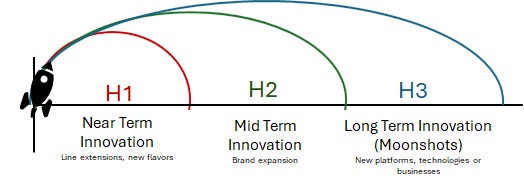

Up until the 1950’s Proctor & Gamble (P&G) was a candle and soap company. One company in a sea of similar household good manufacturers. But in the late 1950s something radical happened. They developed disposable diapers, just as busy, post-War moms were in need of the convenience. The company skyrocketed.

For P&G, disposable diapers were a moonshot, a big bet on a new technology and category. Today, when we think of moonshots, we often think of tech companies and their outrageous big bets, but CPG was once the king of moonshots. In fact, many of the biggest companies in CPG today got there through moonshots, but not anymore. What happened?

In 2024, many big CPG companies are hamstrung by their own size and responsibilities. Once seen as bold risk takers, these companies have aged into safe, reliable blue-chip cornerstones of retirement accounts. Moonshots are risky, unnecessary ventures when you are expected to deliver single-digit growth every year. So, for many, breakthrough innovation has become too costly when new flavors and forms are enough to satisfy the modest growth expectations of the Street.

However, the dependable ROI of big CPG has been shaken. Small brand growth, private label innovation, consumers’ boredom with brand offerings and inflation has all put a dent in big CPG dominance. Now steady growth isn’t as assured in categories that are over-saturated with able-bodied competition. Big CPGs desperately need a moonshot to move them to greener pastures. The problem is, for many, the old moonshot muscles have atrophied. While some think they can buy their way out via M&A, the cost of integration and stronger anti-monopoly regulation are making this more difficult every year.

Strangely, I partly blame P&G. After developing Swiffer in 1999, the company propagated a sanitized myth around that product’s creation, a TED Talk-like narrative of a eureka moment. They said it all originated with researchers watching a video of consumers mopping and the insight that mops ‘just moved the dirt around.’ Then, as though by magic, a billion-dollar new category was created (or at least that’s what people heard).

While that seems silly, you don’t know how many times I’ve been on a call with a client when they’ve told me they need a ‘Swiffer moment’ in their project to unlock growth. This myth, that somehow all you need is a single ‘aha’ insight, has seriously warped innovation expectations (I call it the “Innovation Delusion”). When companies have repeatedly failed to replicate their own ‘Swiffer moments,’ H3 innovation efforts get defunded, innovation groups shut down, and companies retreat to ‘safer’ strategies (i.e., can we change the flavor or make the product ‘mini’?).

The truth is most big CPG companies are awash with ‘Swiffer moments’ everyday but they don’t have the culture to turn them into $B new categories. Insights and ideas must fall on fertile, well-tended ground in order to grow. A single ‘aha’ without the will and mechanisms in place to propel a moonshot will die quickly (often without acknowledgement).

In fact, most big CPG companies (i.e., low variability, steady return) are designed to kill moonshot projects (high variability, uncertain returns). Yes, companies like to say they are all for ‘blue sky thinking’ and ‘white spaces,’ but the truth is the very DNA of these companies has been engineered to squash moonshot initiatives quickly. An idea doesn’t fall in a known P&L = KILL. The forecast doesn’t match the growth trajectory of established SKUs = KILL. Sales are reaching a new target market but cannibalizing a current line=KILL.

CPG employees and groups are trying to innovate and their very own systems and cultures are holding them back.

What will it take to bring back the moonshot? Either very strong leadership or pure desperation. Either could break the delusional fever dream that things will ‘go back to normal’ for big CPG and profits will somehow stabilize. Something must shake existing thinking and introduce the radical change necessary for a reorg for the future.

This could include:

· Building a culture and system that nurtures (rather than kills) real innovation AND keeps the engines running on the corporation’s core businesses

· Tying leadership compensation to building an innovation culture (not a Potemkin Village) and supporting H2 and H3 efforts

· Pausing profit return in favor of plowing it back into a moonshot initiatives (with smart vocalization to shareholders on the long-term strategy to get there—to avoid stock fall off)

The CPG industry is heading for dark times. ‘Profitable volume’ will become the new buzzword as price alone becomes hard to achieve; some companies will not survive. My hope is that insightful leaders will step up and use these desperate times to make CPG companies smart moonshot makers once again.

Humble Brag: The Premiumization of the Ordinary

While the overall vertical farming category is seeing a slump, US-based Oishii (Japanese for ‘delicious’) just raised $134 million in Series B funding. Available currently in the Northeast US, Oishii offers extremely flavorful, premium strawberries and tomatoes. The fruits favor quality over quantity, with the strawberries going for ~$15 for a package of 6. Oishii offers Omikase and Koyo strawberries and Rubi tomatoes. Available at East coast 99Ranch, Whole Foods, and specialty retailers as well Central Market stores in Texas.

Singapore-based startup ButterDays is ready to launch their debut line of flavored butters. The butters are a blend of cultured European tradition with Asian flavors in three varieties: Kimchi Butter, Kombu Butter, and Ube Butter. All butter is currently sold out and there is a waitlist.

UK-based All Thing Butter has a line of “heritage butter for modern foods.” Beyond Salted and Unsalted, the twice-churned, organic and colorfully packed butter is available as Chilli and Garlic & Herb. Available via Sainsbury’s, Ocado, Modern Milkman, and GoPuff.

Massively popular FishWife Tinned Fish and equally popular Fly By Jing have partnered again to release a combination of their well-known products. First is a gold-label addition of their Smoked Salmon with Sweet & Spicy Zhong to celebrate their third anniversary of partnership. New this year is Smoked Salmon with Fly By Jing Chili Crisp. Available online at multiple retailers in US and Canada.

Convenient packaged sauce maker Haven’s Kitchen is out with a new line of flavored aiolis. Made with chickpeas, not eggs, the aiolis are seasoned with vegetables and spices and come in the brand’s ‘low-impact, easy-squeezy packaging.” Available varieties include Sunshine Chili, Zesty Jalapeno, and Herby Yuzu. Available at US retailers and online.

Startup founder Sophia Cheng is launching Oddball this month. A premium, vegan competitor to Jell-O, Oddball draws on Cheng’s experience growing up in Asia eating traditional ‘jellies’ made with agar, konjac gum and fruit. Oddball will be available in four flavors (mango, double berry, grape and pink grapefruit), contain 50 calories per serving, and is made with fruit purees and fruit juice concentrates.

So What? According to a NYT article last week, the most trendy thing on fine dining menus today is… cabbage. How did something so humble and ordinary become today’s ‘it’ vegetable? Part of it has to do with the popularity of its diminutive cousin, the Brussels sprout, and the rise of kimchi into culinary fame. However, much of its recent success might stem from chefs’ renewed interest in pairing the simple vegetable with much bolder partners. For example, the NYT article talks about restaurants serving cabbage with ‘nudja (a spicy pork sausage spread from Italy) and taleggio fondue or creating specialty varietals like Caraflex cabbage. All of which has led to cabbage small plates going for $20+. Once a vegetable of desperate times, households now making $100K+ eat more cabbage than those making <$25K.

We live in interesting times. While classically premium goods are definitely trending (e.g., truffles, caviar, etc.), we are also witnessing a premiumization of the ordinary. What I find interesting is how. Just like with cabbage, the current trend is in the pairing. By smashing together familiar (even boring) products with multicultural flavors and methods, brands are able to ask a lot more for basic goods.

I’ve mentioned this is previous newsletters, but I think we’ve hit a wall with refreshing a category with health & wellness alone. Consumers want flavor with their fitness. Yes, make it vegan, gluten-free or low calorie, but you have to bring the excitement too.

GUT REACTION

TIDBITS

· The fascinating and amazingly complex Waffle House ‘Magic Marker System’ (Note to self, I would not be competent to work at a Waffle House.)

· Costco’s are getting sushi counters

· Target is launching a new paid membership, Circle 360, next month. It will offer free same-day delivery for $49 per year.

· Applebees and IHOP to launch cobranded locations

· Sweden has days of every month devoted to specific pastries

· Novo Nordisk says they have a new drug that is much better at weight loss that Ozempic

· The Hottest Ticket in American Dining: an Applebee’s Weekly Pass

· Aldi plans to add 800 new stores across US

· Apparently, you can make wine with Mtn. Dew

· Denny’s in Japan is not what you’d expect (Exhibit A: a wine selection)

· Return to office policies are leading to a boom in office etiquette training

· Liquid Death now has a valuation of $1.4B

· Lessons learned from Smashmallow’s rise and fall (TOP LESSON: Don’t underestimate the need for rigorous R&D)

Hi, we'd love for you to at least credit us from ripping from our newsletter, that Oishii image is something we put together! It's very clear you're using our newsletters and past issues as reference. https://www.snaxshot.com/p/genzs-not-buying-kylies-rtd