Food Stuff by Kevin Ryan

Private label strength is shaking up the CPG world

Here is a link to my last newsletter, in case you missed it.

In this week’s issue:

Shadow Consumers: The unspoken consumers making you profitable

3 Food Truths & a Lie: A fun food trivia game

Private Label Surges: What can CPG companies do?

Gut Reaction: My quick take on the best (and worst) in new launches

Value & Values: Consumers aren’t paying for sustainablity

Tidbits: The latest in food industry news, from the profound to the funny

Shadow Consumers

Organic cookie maker Emmy’s Organics has launched a new line of Trail Cookies. The vegan, gluten free cookies are made with <12 ingredients and are soft-baked with an oat-base. Varieties include Lemon Blueberry, Apple Cinnamon and Almond Cranberry.

Nature Valley has launched a new range of Soft-Baked Muffin Bars in the UK. The “pillow soft” bars come in packs of four and are made with whole grain. Currently available in two varieties (Lemon Poppy Seed and Chocolate Chip) at Morrison’s and Sainsbury’s.

NY-based chef Zoe Messinger is launching a new brand of sophisticated gelatin desserts called Gelée. Made with freeze-dried fruit powders and beef gelatin (stemming from Messinger’s “obsession” with bone broth). The new offerings (meant for sweet as well as savory, aspic-like meals) come in three varieties, Piña Coco, Passion, and Guava Nectar. Available on the brand’s website.

7-Eleven has announced that they are launching two new lines of energy and hydration beverages: 7-Select Fusion Energy and 7-Select Rehydrate. Fusion Energy contains Vitamin C and B6 and B12 vitamins and has zero sugar or artificial colors. 7-Select Rehydrate has a blend of five electrolytes and vitamins.

EQUII, the protein known for making complete protein breads and baking mixes, is launching a new line of pastas. The company, that utilizes a fermentation process to increase the nutrition of wheat flour, is offering a Rigatoni (28 grams of protein, 10 grams of fiber, and 30% less net carbs per serving and Mac & Cheese (9 grams of protein, 6 grams of fiber, and 33% less net carbs per 3.5oz serving). Available on the brand’s website and Amazon.

Indian sauce brand Masala Mama is launching a new line of pouched, sauced beans. The plant-based, gluten free, certified organic products are made with avocado oil. Varieties include Ooh La La Lentils, Cha Cha Chickpeas, Rah-Rah Red Beans and La Bamba Black Beans. Available online and at Whole Foods and regional US natural retailers.

So What? When you manage a brand, it is important that you know your main consumer. Their changing tastes and concerns can mean the difference between skyrocketing growth or a quick decline. However, digging into the numbers, you’ll often find that there are niche groups of consumers that (at least cumulatively) make up a large amount of your overall volume. I call these shadow consumers.

While you might not talk about these consumers or even target them in your messaging, their spend is often critical to your business. Take LEGO for example. While the brand is primarily centered on sparking creativity and joy with children worldwide, less well-known is that the brand sells a lot of blocks to adults. In fact, Adult Fans of LEGO (AFOL) are a very important fan base for the brand which the company supports by sponsoring conventions, outreach, and occasionally launching limited edition sets intended specifically for adults.

In a similar vein, there is the South American superfood quinoa. While it would be correct to assume that the majority of quinoa is purchased by wellness consumers for their protein-rich grain bowls and breakfast porridges, there is a shadow market that is much less discussed: dogs. With the rise in grain-free dog food, a growing amount of quinoa is being sold through pet stores.

I say all of this because there is a connective force among today’s trendy foods and beverages that might be driving brand growth: aging consumers.

When people age, we know the following can occur:

· They lose their sense of taste and smell and gravitate toward bolder flavors and enhanced textures

· They have dental issues (loss of teeth, dentures) and migrate toward softer foods

· They have slower digestions which results in a need for more fiber and probiotics for regularity

· A loss of muscle mass (sarcopenia) and an increased need for more protein

· A higher risk of dehydration because of the decreased sense of thirst

· Lower energy due to a series of cognitive and physical factors

I don’t know about you but, when I see this list, it looks a lot like a checklist for the most popular benefits of the last 3-5 years: high protein, gut health, soft-baked, bold flavor, hydration, and energy.

I don’t think this is an accident. While brands might not be specifically aiming at aging consumers, as the Western consumer base ages, the benefits that resonate are bound to rise to the top. Mitigating aging issues has become a ‘shadow’ benefit for more consumers.

This is not to say that brands should pivot to aggressively message to aging consumers, but that there may be a benefit in considering how much these consumers are adding to the bottom line. Perhaps there is a way to utilize target marketing and messaging to increase your reach or even consider spinoff products and brands to appeal to them.

3 FOOD TRUTHS AND A LIE

Which one of the following food facts is not true (see bottom of newsletter for answer)

1. When originally testing the use of Wi-Fi on commercial airplanes, Boeing used sacks of potatoes in place of passengers.

2. An upscale Korean butcher shop in Manhattan is now offering wagyu beef wrapped in silk

3. Pepsi once owned the 7th largest naval fleet in the world

4. A mixologist in California is trending by making drinks with mint plants that were watered with 7-Up (and developed a distinctly lemony-mint flavor)

A Disturbance in the Force: The Revenge of Private Label

Walmart’s Bettergoods brand has launched Chef-inspired Smoked Gouda Mac N’ Cheese flavored potato chips. Available in an 8-oz bag either in-store or at Walmart.com.

Frito-Lay has launched an LTO line of potato chips in the US that celebrates flavors from around the world. Flavors include Wavy Tzatziki (Greece), Masala (India), and Honey Butter (Korea). The chips are being marketed with an on-bag QR sweepstakes offering one consumer the chance to visit one of the flavor origin countries.

The fan favorite noodle now has a spicy spinoff. Trader Joes has launched Spicy Squiggly Knife-Cut Style Noodles. The 4-pack of dried noodles comes with a packet of Spicy Garlic Sesame Sauce to drizzle over. Available now at Trader Joes.

To appeal to the bold taste desires of Gen Z, Kraft is launching two new flavors of their classic Mac & Cheese, Jalapeno and Ranch. The company says they went through “27 flavors and 40 different concepts” to arrive at these two varieties.

In time for Fall, Target’s Favorite Day brand is launching Hot Chocolate Drops. The kiss-shaped candies are made of Belgian chocolate with a center of dissolvable cocoa. The brand recommends dropping them into hot milk or eating them straight from the bag.

Hershey’s is launching new candies that are tailor-made for trick-or-treating. The new snack-sized offerings include Kit Kat Ghost Toast (crispy wafers covered in a cinnamon toast-flavored crème) and Reese's Werewolf Tracks (vanilla-flavored creme with milk chocolate and peanut butter).

Organic nut butter-maker Once Again is launching Chocolate and Peanut Butter Filled Graham sandwiches. Packaged two to a pack, the gluten-free, non-GMO sandwiches are made without palm oil.

Trader Joes has launched Crispy, Crunchy Coated Peanuts. Based on a classic Japanese-Mexican confection (cacahuates japoneses), the snack consists of a sweet soy sauce-infused wheat coated shell on dry roasted peanuts.

So What? Last week, P&G and Nestle announced quarterly numbers and both CPG brands said they were seeing slowdowns in sales due to rising private label compeition. At the same time, Walmart announced a surge in sales coupled with a cut in prices.

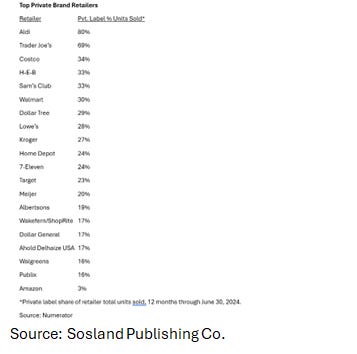

New data from Numerator’s Private Label Trends Tracker shows that grocery’s private label unit share for the first half of 2024 was nearly 24%, up 0.5% from a year ago. The numbers revealed that Walmart’s private label brands have the highest household penetration of any retailer—with Great Value in 86% of homes (but Kroger’s new Smart Way is the fastest growing PL brand). However, the real shocker comes when you start looking at how much private label accounts for units sold in each retailer.

To put this into context, private label averaged about 14% in the late 1990’s in the US (peaking at 17% during the economic downturn of the 1970s). Once thought impossible, we are now seeing the US trending toward EU or UK levels of private label penetration (~35-45%). In fact, I believe it is the growing fear of this retail existential crisis that is motivating many of the moves we are seeing from major CPG companies (e.g., Mars acquisition of Kellanova). Major food companies are gathering forces to compete against the growing private label strength across the globe.

So how did major CPG companies, once the reigning category captains, let it come to this and how will they fight back? I see 6 forces at play:

1. Lean times + CPG margin structures: Let’s start with the most obvious reason for private label’s recent increase in popularity, groceries are just more expensive. When times are tough people often go searching for lower cost options and today is no different. However, this time the difference between private label and CPG seems especially stark coming out of a period where large brands took cost 2, 3, and even 5 times. Whereas previously, the cost difference between CPG brands and store offerings was just pennies, today it isn’t unusually to see a 20-30% difference. This delta is compelling enough to shoppers to justify the trial of private label (and potentially never return).

CPG Imperative: Brands must rethink their margins. For many corporations, this is an almost inconceivable option, margin structure dicates all. However, when competing against a foe that is able to comfortablely sell at 1/3 the price, something must be done. With the market looking to publicly traded CPG companies for healthy returns, the math is clear. There is a reason that Mars is in the news recently with their acquisition of Kellanova. Mars’ private ownership gives it much more latitude and speed in these matters. Therefore, for the public CPG companies, Mars is just as dangerous as private label.

2. Loss of brand differentiation: Speaking of margins, keeping them high for big CPG companies has also led to significant changes in product quality and shrinkflation. As cost of goods and transportation have increased, iconic brands have been slowly removing differentiating benefits from their products. Of course, this wasn’t done on purpose, but over time the removal of small product factors have impacted the overall experience. Cheaper product B may be just as preferred as Original product A, but cost-saving creep means that by the time you get to reformulation Z it bears little resemblance to Original product A. This loss has been private labels gain. Lacking its original ‘uumph’ , private label becomes more alluring.

CPG Imperative: Like the Ship of Theseus, it is hard to pinpoint what portions of the original branded product were really needed to make it special and loved. Cost-savings removed and modified ingredients and packaging systematically, but consumer experiences are holistic. Companies need to do considerable research and soul searching to understand the experience they inadvertently removed and, in turn, ‘add back the magic’ without the costs.

3. The Toolbox is Open: For years, one of the barriers to entry for startups and private label was not having access to the technology that made iconic brands special. ‘Generic’ Pop Tarts and Shredded Wheat just didn’t taste right because it was made with different equipment. However, as patents expired and heritage experts were removed in CPG corporate downsizing, suddenly co-manufacturing has become increasingly better. Private label is now able to tap into this manufactering network and produce products with qualities previously only seen in big brands.

CPG Imperative: If you look at most other industries, the percentage of investment in R&D is often orders of magnitude higher than CPG. In pharmaceuticals, R&D investment is ~16 of revenue spent, in computers/electronics its ~13%, and chemical companies ~8%. For food companies, the average is < 1% of revenue spent (NSF and CBO). Many big food companies are leveraging decades old IP to run up against retailers. However, that well is quickly running dry. There is a desperate need for CPG companies to make large, targeted investments in R&D programs and lock up the resulting IP. To do this, companies need to run thorough innovation exploration and priortization programs (e.g., Opportunity assessment, JTBD, etc.) to know ‘where to dig’ in the future.

4. Own the Experience: While big brands might make the products, it’s the retailer that is there at the first moment of truth. This didn’t seem that important years ago when brands saturated consumers’ lives with mass media advertising, but as media has splintered into hundreds of channels, the IRL touchpoint has become especially important. Couple this with retailers’ move to app-based shopping (either for delivery or hybrid in-store) and the strength of the retailer relationship just increases.

CPG Imperative: Brands must find ways to maintain and enhance their emotional resonance with consumers. If retailers own the bottom of the funnel, then CPG companies must do their best to own the rest. This is likely where AI tech and smart advertising personalization become important. If brands can appeal to consumers in a personal way all the way up to the point of purchase (and after) then they can guard against the emotional appeal that retailers exert in-store.

5. Short Attention Span Excitement: Companies like Target and Walmart have reverse engineered the appeal of Trader Joes and extracted the formula for consumer love—give shoppers exciting, novel products at a rapid-fire rate to maintain attention. The reason why this strategy is so effective is, not only does it resonate with the attention span of today’s social media consumers, but it also sits in a weak spot for large CPG companies. Structured to produce a few ‘big bang launches per year’ and then make these products more efficiently than others, big brands struggle with the rapid pace that retailers like Trader Joes (and now Target and Walmart) maintain.

CPG Imperatives: See below

6. Not Afraid of Niches: The fast pace of private label launches, and ownership of the channel, allows retailers to try flavors and forms that big CPG would never gamble on. Today’s consumers are exploring much more diverse and unique universes of food/bev and are looking for these represented in their grocery store. While deep, these niches of consumer interest are narrow, and are often seen as not worth the effort for big CPG brands. While this is sound thinking, it also means that big brands miss the phenomena that start small but rapidly expand. By the time brands try launching their versions, consumers see it as passe and already see five small brands in the space.

CPG Imperative: Many CPG brands have been playing around with their own small brand incubators or investment arms for years now. However, many have failed to bear fruit. Instead, it might be time for brands to re-investigate and invest in radical speed to market initiatives. Not only the WHAT (e.g., agile, in-market testing, etc.) but also the HOW (e.g., rapid and flexible manufacturing, micro-scale production, etc.). The ‘tent pole’ strategy of many brands needs to be supported with a much nimbler in-and-out strategy to keep up with today’s consumers and private label. This would also allow brands to test out the waters on more niche offerings.

GUT REACTION

Value and Values

KFC Thailand is introducing a limited-edition reusable, microwave and freezer safe KFC Bucket Ware for Mother’s Day. The promotion, which shows consumers using the container not only for leftover chicken but also uses around the home, is in partnership with the Thai brand Super Lock.

Nespresso is launching their first non-coffee SKUs with Coffee Blossom Honey. The new honey is harvested from hives on the same Columbian land Nespresso grows their coffee beans. Nespresso is marketing the honey (and honey syrup) not only as perfect compliments to their coffee but also as a great way of supporting the bees that make the coffee possible.

DE-NADA Tequila is introducing new packaging for their carbon-neutral, eco-friendly spirits. The new bottles are made of aluminum together with a 100% sustainable cork topper. The bottles are significantly lighter than glass and the company says the spirit retains better quality .

So What? In surveys, everyone loves the environment, until they have to open their wallets.

Consumers want greener choices but often think brands should absorb the costs. Of course, with margins already shrinking , this is very difficult to do except for premium offerings.

The way around might be to offer more. If you can provide not only an environmental benefit but also a value, convenience or taste benefit, you can give consumers a functional reason to pay more to go with their heart.

TIDBITS

People into mewing (the TikTok craze to strengthen your jawline) now have special gum, does it work?

The 33 new food offerings at this year’s Minnesota State Fair (the best fair in the US)

Australia starts world’s-first nationwide peanut allergy treatment for babies

The Din Tai Fung Soup Dumpling Index (i.e., how many dumplings do you get in each city for $10)

The sudden rise of Type 2 diabetes in children

Who benefits from convenience stores locking up merchandise? Amazon, apparently

Kraft-Heinz investing in a new sugar that turns to fiber in your gut

Scientists are trying to making nuclear fusion more efficient—with mayonnaise

Taco Bell is a bright spot, but Yum’s Pizza Hut and KFC see dwindling same store sales

McD’s is still on top, but Chick-fil-A is amazingly efficient at making cash

McDonalds goes nostalgic by bringing back collector water glasses with equity characters

Corporate cafeterias aren’t working anymore according to a new survey

How cattle feed led to the creation of cheese puffs

Eli Lily made $1.4B more than estimated in the second quarter as sales of weight loss drugs Zepbound and Mounjaro climb

Korean Air has announced they will no longer be serving instant ramen on flights due to the chance of burns during turbulence

Court rules Coca-Cola must pay ~$6B to the IRS in back taxes, and could end up owing $10B more

In case you were wondering, yes you can make ice cream from horse milk

Passes for Taco Bell’s early, early retirement center (The Cantinas) sold out in three minutes

Labelling consumer goods as using AI in the product description significantly lowered consumer trust in the product

The Hotdish Ticket, the food-centric combo of the Harris-Walz campaign

Chuck E. Cheese creates a subscription service

Impossible Foods opens first concept restaurant in Chicago

How the online craze for Swedish candy rocked global supply chains

Celebrity coffee is the next celebrity tequila

Tesla has enter the candy industry(?)

Have an allergic reaction to food eaten in a Disney park? The contract you agreed to when signing up for Disney+ might prohibit you from a jury trial

Your microwave has its own microbiome (which, I guess, is just its biome then)

Hello Fresh is growing again

Cultivated meat company Upside Foods sues Florida saying ban on the tech is unconstitutional

Where more people in the USA are WFH

Speaking of WFH, soon to be Starbucks CEO Brian Niccol will receive ~$117m in his first year, a $10m sign-on bonus and can work from home.

Food Truths and a Lie Answers

1. True; Potatoes have similar water content to humans and absorb electromagnetic waves like us

2. True; meat is selected with a specialist, wrapped in silk fabric with tassels and vacuum sealed.

3. True; During the Cold War, the Soviet Union paid Pepsi with 17 submarines, a cruiser, a frigate, and a destroyer (all decommissioned) which on paper made them as big as the Indian navy.

4. False; please don’t water your mint (or other plants) with anything but water