Culture Matters

Is the end of cereal near? Plus, what does Mondelez's closure of their internal startups mean for the industry?

In today’s newsletter:

Cereal Armageddon: The Final Bowl?

New Age: Why Longevity is the trend for future

Startup Trouble: Why big CPG companies has so much trouble with internal startups

Tidbits: Quick links to fun and interesting food news

Did you miss the last newsletter? Find it here

Can Cereal Survive?

German cereal maker Kölln has introduced a new line of vegan chocolate-based muesli cereals. The muesli contains the cocoa-free chocolate alternative ChoViva, made from a patented fermentation process involving oats and sunflower seeds. The new cereals are available at Rewe stores in Germany in three varieties: Crunchy Waffle, Crunchy Hazel and Crunchy Berry.

Iowa-based Hy-Vee supermarkets are launching a limited-edition version of their private label wheat flake cereal honoring Jack Trice, Iowa State University’s first Black athlete. A portion of each cereal sale will be donated to the Trice Legacy Foundation, offering scholarships and technology grants for Black students pursuing college education.

General Mills is debuting a Halloween edition cereal. The two-bag box contains a Kit Kat cereal and bat-shaped Reese’s Puff. The cereal is a Sam’s Club exclusive.

Cereal maker Catalina Crunch is introducing a new Pumpkin Spice variety of its Keto-friendly cereal. The cereal is made from a non-GMO blend of plant proteins and fibers, contains 11 grams of protein, 9g fiber per serving, and zero sugar.

So What?

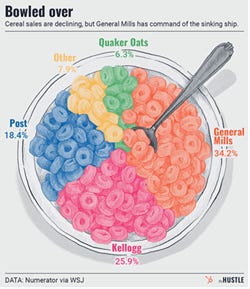

The Wall Street Journal had an article last week that spelled out what many in the food industry have already known for some time: the RTE breakfast cereal category is dying. The pandemic uptick in cereal consumption, which in 2021 was hailed as a category reinvigoration, is now looking more like a dead-cat bounce.

So, what will happen to a massive category that dominates entire aisles at most US grocery stores? Can it be saved? Who can save it and how? Currently, General Mills is leading the growth in the category, but can it reverse the overall decline?

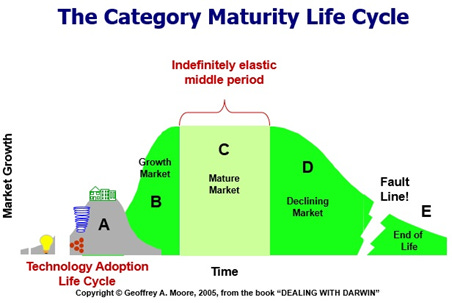

For potential answers, I went to Geoffery Moore, management consultant and author of the great 2008 book, “Dealing with Darwin.” While his writing talks mostly about tech, I think there are a lot of similarities to CPG. Moore maps out a category’s life cycle like this:

As categories enter decline, the following tends to happen, and is happening in the cereal category (paraphrasing Moore):

Context Over Core: As a category matures, more companies are likely to focus on "Context" innovations—efficiency, cost-cutting, etc.—rather than "Core" innovations (activities that directly contribute to a company's competitive differentiation and consumer value proposition)

Commoditization: Companies might lean heavily on Operational Excellence to improve margins. This could lead to greater commoditization as everyone tries to be the low-cost leader.

Exiting: Leading brands find ways to cut their losses and reinvest elsewhere (see Kellogg’s spin off of their cereal business WK Kellogg Co)

Decline in Customer Intimacy: As the market shrinks, brands might focus less on connecting with consumers and more on survival tactics, like mergers and acquisitions.

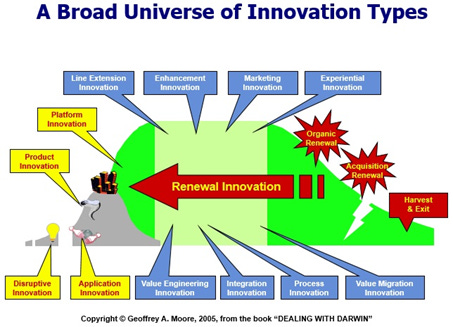

However, it’s when Moore dives into the different types of innovation to use at each stage of the life cycle that we get some potential answers on what could happen to cereal.

To save a declining category, cereal companies should do the following (in fact, many of these show why General Mills is leading):

Revisit Core Innovations: Instead of getting caught up in Context (i.e., cost cutting), brands need to refocus on Core innovations that can redefine their value proposition. This could be radical changes in product formulation, flavor profiles, or even the eating experience (e.g., multi-textural cereal).

Category Renewal: Here the brand needs to think outside of itself and look to innovation that redefines the whole category, potentially subverting consumer expectations. We’ve already seen some of this happening as brands try to turn cereal into a snacks, but there may be other occasions and benefits that cereal could slip into. A good example of this is currently happening in ketchup. Other sauces are getting all the love and ketchup is slowing fading. Heinz is trying to see if there is potential for category renewal (maybe they saw that Rao’s is making ketchup?):

Nichification + Premium: One way forward for the category is to turn away from mass market and become highly specialized and premium. Looking at the data, when consumers with household incomes $150K+ buy cereal, its usually keto and gluten free. There are likely even deeper niches to explore and channel opportunities (i.e., Club).

Invest in Consumer Intimacy: Even in a declining market, there's value in knowing your consumers better than anyone else. Brands can focus on hyper-personalized offerings or loyalty programs that keep their existing consumer base engaged and less likely to defect.

Look for Adjacencies: In Moore’s early book "Crossing the Chasm," he discusses a concept called the "Bowling Alley" where brands need to look at adjacent markets where they can ‘knock down pins’ with their products/brands. Could cereal become a staple in some other type of meal or snack occasion?

Alliances and Partnerships: We are already seeing this as cereal brands partner with ice cream companies, cookie companies and others to create co-branded product lines. Personally, I think digital/social media may be an alliance to further explore. While partnerships are often a one-off, there may be some that allow a cereal brand to escape the aisle permanently.

So, is cereal going away? No, we’ll likely always have cereal. The real question is how long will cereal be as prominant and profitable as it is now?

The Age of Longevity

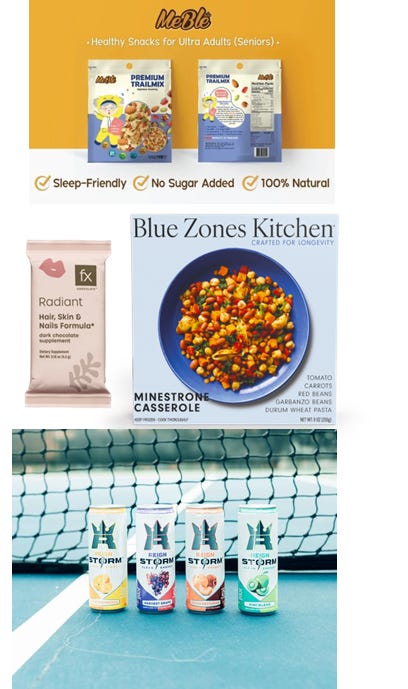

Expo East last week saw the debut of Blue Zone Kitchens, a line of frozen meals co-founded by Dan Buettner, author of the 2008 book Blue Zones, referring to the regions of world with the healthiest and happiest populations. The new meals offer longevity supporting foods inspired by the cultures in the Blue Zones. Products include frozen, plant-based burrito and rice bowls as well as casseroles.

Premiering last week at the international Anuga 2023 show, Chin Huay Public Company announced the launch of premium snack for “ultra adults” (i.e., seniors). The trail mix is optimized for nighttime snacking, featuring super-soft dehydrated mango that's easy to chew and infused with probiotics.

FX Chocolate, a supplement company, has launched Radiant, a chocolate designed to improve hair, skin and nails. The chocolate contains red current, blackberry, and bamboo extracts as well as astaxanthin. Each chocolate has 0g sugar and is non-GMO. Available on the company’s website.

REIGN Storm, a zero-calorie energy drink, has been announced as the official energy drink of the Association of Pickleball Players (APP). REIGN Storm contains a plant-based energy blend “ designed to give those with active lifestyles a guilt-free 'better me' energy surge.”

So What? I always like the quote from cyberpunk author Bruce Sterling who once said, “The future is about old people, in big cities, afraid of the sky.” His point being you can’t outrun the final truth of demographics and science. Like it or not, developed countries are getting older, they are urbanizing and climate change is real.

While all that is true, what constitutes “old” is something else entirely. In the last 20 years, we’ve seen a massive cultural shift in how we think about old age. As the very large cohort of Baby Boomers aged, their enormous influence on society, compared to the smaller, younger generations after them, has managed to reset our culture’s view of aging. Whereas prior generations saw the senior years as a time to leave positions of power or leadership (literally ‘retire’—“to withdraw or exit”), Baby Boomers are pushing hard on past aging assumptions. So, now we hear things like 60 is the new 40 and our top action stars (Tom Cruise, Denzel Washington, and Keanu Reeves), politicians, and CEOs are in their 60s-80s.

All of this is leading to a new conversation on Longevity. Not just living longer but living longer, better. The crux of New Aging, as I like to call it, isn’t about living to be 100 (despite the title of Buettner’s new Netflix show), it’s about staying ‘in the game’ as long as possible. Relevance is the benefit, and it is delivered through mental or physical gains.

One issue with marketing these products is that New Agers don’t necessarily want to call out their senior-ness. That’s why I’m a little skeptical with the long-term success of Blue Zones Kitchens. It’s a little too ‘on the nose’ and putting it into your grocery cart still feels ‘old.’ Also, why would you need to purchase it when there are so many products coming on the market that already aim at delivering mental and physical improvement WITHOUT the stigma. Therefore, the better strategy is to create a product that is age agnostic but micro targeted to New Agers.

Trouble for Internal Startups

Mondelez quietly announced last week that they were winding down the brands they created through their Snack Futures arm. The brands, Dirt Kitchen (a no sugar added pressed fruit and seed bar) and CaPao (an upcycled cacao fruit and quinoa snack), will be phased out of retail distribution by the end of this year. The company told Food Dive that they would focus their efforts on investing in existing external startups versus creating their own.

So What? Why does big CPG have such a hard time starting new brands and supporting internal startups? Personally, I tend to believe that the forces that make a company good at being a successful startup are counter to those that make it a profitable large company. Therefore, putting them under the same roof can cause friction, tension, and with most companies, a breakdown.

1. Culture & Speed: The corporate culture in big CPGs is fundamentally different from startups. Everything in a big company is designed to make sure that things happen at scale, with precision, and with no variability (i.e., they make their money on the fact that the stuff in that bottle or box is exactly the same everywhere, every time). That mindset forms a culture where processes, hierarchies, and a strict way of doing things is the norm. This can slow down decision-making and reduce the agility needed for smaller brands.

2. Risk Tolerance: Big companies have a lower risk tolerance than startups because they have a lot more to lose (i.e., $B’s and thousands of jobs versus $M’s and dozens/hundreds of jobs). For startups, often buying enough inventory to cover next month’s orders is risking the company’s future, therefore making big bets becomes normalized. Big companies have protective layers of risk aversion. They have boards and shareholders who are concerned not only about this quarter’s numbers but the company’s standings in the global economy. This causes big companies to develop a risk culture with checks and balances built into the fabric of the system. StageGate, manufacturing processes, communications—they all have people and rules in place to limit the risk of bad decisions mucking up everything. The downside is that anything new is also flagged as risky—because it is—causing the corporate antibodies to attack and kill it before it catches on.

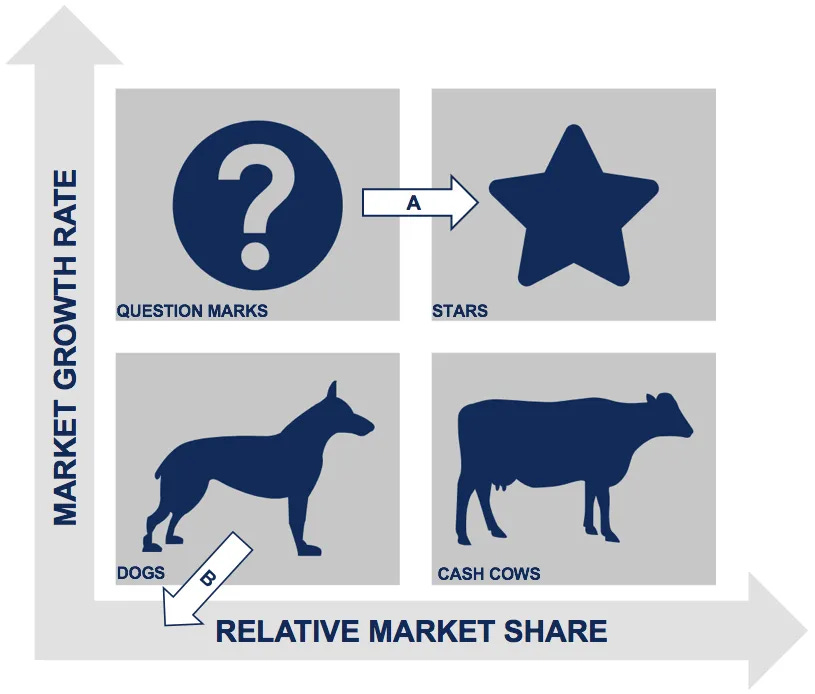

3. Resource Allocation: In large corporations, resources, including budget and talent, might be directed towards already established, star products. This can leave smaller brands fighting for the crumbs. While big corporations seem sophisticated in their strategies, most are still running off of Boston Boxes (aka BCG Matrixes) where only Stars and Cash Cows are celebrated and Question Marks (i.e., internal startups) are either converted to Stars quickly or reclassified as Dogs and phased out.

4. Different Metrics of Success: Startups might define success as user growth, brand awareness, or other non-revenue metrics, especially in the early days (and if they have long-term angel investors, harder to get nowadays). Big CPGs often look at profitability and revenue right off the bat, which can stifle innovative brands that need time to grow. If the C-suite is used to seeing the quarterly profit numbers from $B brands, the struggles of an internal startup seem more like a nuisance than an opportunity.

5. Talent Mismatch: The kind of talent that thrives in a startup environment – wearing multiple hats, moving at a rapid pace, being hands-on— might not always be a fit for a corporate environment, and vice versa. So, corporate startups either end up with (A) disgruntled startup employees who chafe at the corporate culture; (B) corporate employees cosplaying as startup employees (but who are never really into it); or (C) disgruntled corporate employees that like the safety and security of a big company but strive for something more challenging in their role. All of which makes for an HR and talent aquistion nightmare.

6. Market Understanding: Sometimes, big companies can be out of touch with the niches that smaller brands cater to. They might not "get" the target audience or understand the nuances of the market as a nimble startup would. While this can be solved by deep research (often qualitative) with niche groups, this only solves the problem for the internal startup team. Then they need to convince unempathetic leadership that their undertaking not only makes sense but needs a long runway to profitability. In the end, it becomes a marketing problem. Not an external marketing problem, but an internal one.

7. Supply Chain Issues: Big CPGs have supply chains optimized for large-scale production. Adapting to smaller batches and unique requirements of a niche brand can be extremely difficult. You can’t just break into a line making thousands of cases to make your new product that MIGHT sell a few hundred cases. Yes, you can use co-packers, but you’ll likely have to go outside the system and navigate a legal quagmire (see risk tolerance above).

8. Innovation Structure: When larger companies are setting innovation strategy, it’s often in service to their existing business model. You are spending all your time trying to optimize and maintain your current market leadership. Yes, smart companies are told to “disrupt yourself!”, but that only looks good on paper. Imagine if you are a multi-billion-dollar potato chip company and have spent hundreds of millions investing in innovation to maintain your existing lead in the potato chip category (not to mention amortize the millions you just paid for those new potato chip fryer systems). How much money and oxygen are you giving a ragtag team that tells you that they have something that will disrupt potato chips?

This doesn’t mean that internal startups are impossible, just extremely difficult. However, with funding becoming much more sparse in the real world, I think the constant concern that startups are an existential threat to big CPG companies will diminish. This will cause big CPG companies to turn their attention elsewhere for new inputs (e.g., corporate venture capital, accelerator programs, strategic partnerships, open innovation, etc.). Net-net: I think the days of internal CPG startups are numbered.

Things I’m Watching

The speed of a company’s social media group to quickly jump on a viral moment seems to be the metric of the moment. In the last several weeks we’ve seen the following:

1. ‘Girl Dinner’ became a trending meme (and controversy) with companies like Popeye’s offering their take (and Lunchables vying for ‘Guy Dinner’)

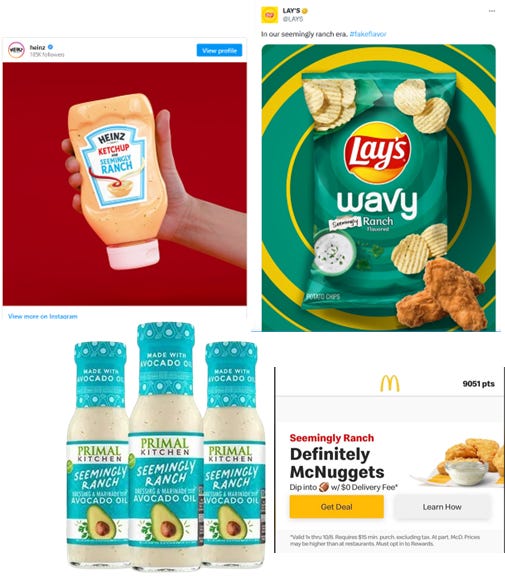

2. Taylor Swift, Travis Kelce, Kansas City Chiefs and ‘seemingly ranch’ (read about it here if you are out of the loop). This caused everyone from Hidden Valley Ranch and Primal Kitchen (understandable) to offer actual products, to Lay’s offering a fake one, and McDonald’s just being cheeky.

3. The Roman Empire meme, where people asked their male partners how often they think about the Roman Empire (a lot it turns out). This caused Panera to launch an online ‘Roman Empire Menu’ of items “…you just can’t stop thinking about!” However, the offerings weren’t new or Roman related, just popular like Cinnamon Crunch Bagels and Chipotle Chicken Avocado Melts.

The question is: do brands need to have a comment on all these viral moments? I actually thought most of the above were good (although the Panera one was…random). However, it makes me wonder if brands have a checklist of what they will respond to versus what they’ll ignore. Things like relevence and authenticity (to the brand and topic), sensitivity and understanding (of the audience and the meaning of the meme), and timing and saturation have to be considered. My point being, these ‘viral moments’ are only going to become more frequent (daily, hourly?), and brands will need to be more choiceful with what conversations they insert themselves into.

Once Upon a Farm has launched a new line of refrigerated oat bars for kids. The new bars (available as Strawberry, Banana Chocolate and Apple Cinnamon) are being marketed as a no-spoon required version of overnight oats. Each bar is made with fruits and veggies and has a no-sugar drizzle. Available in Target and Wegman’s as well on the company’s website.

So What? There are quite a few reasons why refrigerated bars make more sense for Once Upon a Farm than traditional adult bar brands. First, parents are more likely to be concerned about food additives and freshness for their kid’s food than even their own. Second, the premium price for a refrigerated bar is more in line with organic toddler and kid food (i.e., an easier transition than moving ambient, non-organic snack bar users to the refrigerated space). Lastly, Once Upon a Farm is already in the refrigerated case with pouches so it’s not a new habit for current consumers—that was a problem with refrigerated bars. (the brand even sells a pouch cooler).

If anything, this move shows the brand’s aging up ambition. Just as Annie’s started as a kid’s only brand and has now widened its target to gain incrementality (“Organic for EveryBunny”), Once Upon a Farm looks to be headed in the same direction (not a surprise, both brands have overlapping smart leadership in John Foraker). While I don’t think Once Upon a Farm is headed for all-family offerings just yet, I can see them working up from adolescents, to tweens, then teens as they expand their line.

TIDBITS

How we’ve come to fetishize the color of egg yolks

French supermarket chain Carrefour is calling out Pepsi and others (on shelf!) for shrinkflation

Who knew shot glass standards were so different around the world? (i.e., remind me not to do Țuică shots with Romanians!)

Beyond bees: new research shows that earthworms contribute greatly to grain production

Hurricanes and weather trigger record prices for orange juice

Relatedly, amazing drought-friendly fruits and vegetables are coming

Lawsuits are mounting against fast food companies saying the food doesn’t look as advertised

Which country has the most “best restaurants in the world”?

Alicia Keys files trademark for new beverage brand “Alicia Teas”

Rapper Wiz Kalifa starts mushroom company

McDonald’s says they are getting rid of self-service soda machines citing declining dine-in numbers

Blue Apron to be acquired by Wonder Group for $103 million

The science behind why we eat so much at the movies

Heart-warming and engaging story of the role of food and dementia